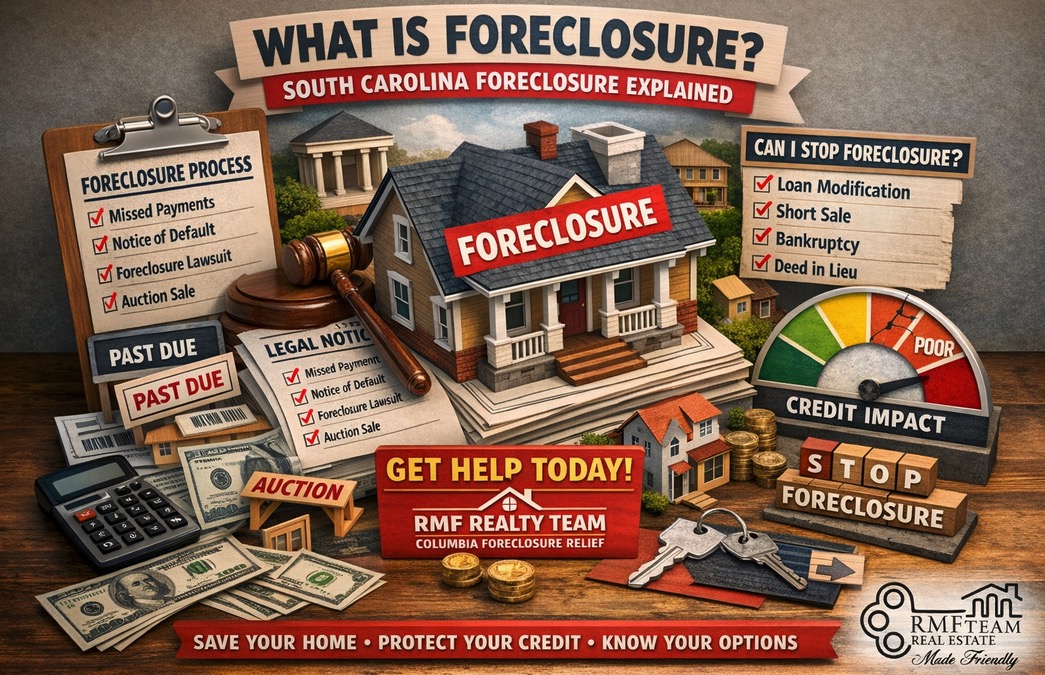

What Is Foreclosure?

If you’re asking, “What is foreclosure?” you are not alone. South Carolina Foreclosure cases are rising as homeowners face job loss, divorce, rising insurance premiums, HOA liens, and unexpected financial hardship. Understanding how South Carolina Foreclosure works is the first step in protecting your home, your credit, and your future.

At RMF Realty Team | Columbia Foreclosure Relief, we believe education creates options — and options create solutions.

🎥 Watch the Video Above

Foreclosure is a legal process that allows a lender to take back a property when a homeowner fails to make mortgage payments as agreed.

In South Carolina, foreclosure is a judicial process, meaning the lender must file a lawsuit in court before the property can be sold at auction.

This is important because:

✔️ You are served legal documents

✔️ You have the right to respond

✔️ A judge must approve the foreclosure

✔️ The property is typically sold at a public auction

How Does Foreclosure Work in South Carolina?

Here’s a simplified breakdown of the South Carolina Foreclosure process:

Missed Payments – Typically after 3–4 months of missed payments.

Notice of Default – The lender notifies you that you’re in default.

Foreclosure Lawsuit Filed – You are formally served court papers.

Court Judgment – If unresolved, a judge issues a foreclosure order.

Auction Sale – The property is sold at a courthouse auction.

Possible Deficiency Judgment – If the home sells for less than owed, you may still owe the balance.

⚠️ Many homeowners don’t realize they could still owe money even after losing the home.

Two Critical Questions Homeowners Ask

❓ Can I stop foreclosure once it starts?

Yes — in many cases.

You may qualify for:

Loan modification

Forbearance

Repayment plan

Short sale

Deed in lieu of foreclosure

Bankruptcy protection

The earlier you act, the more options you have.

❓ How will foreclosure affect my credit?

A foreclosure can lower your credit score by 100–160+ points and remain on your credit report for up to 7 years.

However — recovery is possible. With the right strategy, many homeowners can purchase again in as little as 2–4 years depending on loan type.

Why South Carolina Is Different

Unlike some states, South Carolina Foreclosure requires court approval. This means there is often time to:

✔️ Negotiate with the lender

✔️ Explore a short sale

✔️ Avoid a deficiency judgment

✔️ Protect your equity

✔️ Plan your next move strategically

Time is leverage — but only if you use it wisely.

Warning Signs You Shouldn’t Ignore

You’re 60+ days behind on payments

You received certified mail from your lender

You were served court papers

HOA foreclosure notice

Property tax delinquency notice

If any of these apply, Do Not Wait!

Your Options Matter

Foreclosure is not just a legal process — it’s emotional, financial, and deeply personal. I’ve worked with homeowners across Columbia and the Midlands who felt embarrassed, overwhelmed, and unsure where to turn.

You are not alone — and you have options.

At RMF Realty Team | KW Preferred, we specialize in:

✔️ Pre-foreclosure solutions

✔️ Short sale negotiation

✔️ Deficiency judgment guidance

✔️ Divorce & foreclosure crossover cases

✔️ Strategic exit planning

We focus on protecting your dignity, your credit, and your future.

Don’t Wait Until Auction Day

The biggest mistake homeowners make? Waiting.

The sooner we evaluate your situation, the more control you keep.

📞 Call or text today

📩 DM “RELIEF”

🌐 Visit Columbia Foreclosure Relief Contact Us Today!

Guiding You Home with a Smile — Even Through Difficult Seasons.

#SouthCarolinaForeclosure,#ColumbiaSCRealEstate,#ForeclosureRelief,#StopForeclosure,

#ShortSaleExpert, #ColumbiaForeclosureRelief,#DeficiencyJudgment, #RMFRealty,

#MidlandsSC,#PreForeclosureHelp,#RMFRealtyTeam,#GuidingYouHomeWithASmile,